Logistical Challenges of Moving a 529 Plan to a Roth IRA

The Deep Dive:

Starting in 2024, families gained a powerful new planning lever:

You can roll unused 529 funds into a Roth IRA for the beneficiary.

That sentence sounds simple.

The execution is not.

If you want to use this correctly and avoid penalties, misreporting, or lost contribution years you need to understand the mechanics, the limits, and the tax reporting trail.

Let’s walk through this step-by-step.

The Law That Made This Possible

The change came from the SECURE 2.0 Act.

It allows tax-free rollovers from a 529 plan to a Roth IRA for the beneficiary of the 529, subject to very specific rules.

They made sure that this is not a loophole. It is a tightly structured rollover provision with guardrails and penalties for mistakes.

Step 1: Confirm Eligibility (Before You Touch the Account)

There are five non-negotiable rules.

1️⃣ The 529 must have been open for at least 15 years

This is account-level aging not beneficiary aging.

If you changed the beneficiary recently, we are still waiting on clarity from the IRS about how that affects the 15-year clock. Conservative planning assumes a reset risk.

If the account is 14 years old and 11 months, you wait.

2️⃣ Contributions made in the last 5 years cannot be rolled over

Any contributions (and associated earnings)made in the last 5 years are excluded.

This means you need contribution history.

Not guesses.

Not “about.” Exact records.

In particular, the associated earnings in the last 5 years of contributions can be tough to track down. If you have been taking distributions out of it, while contributions (for state tax deductions), it gets very tricky to break this out. Year end statements are your best bet to build an argument that the amount you are moving over does not come from contributions and growth on those contributions in the last 5 years.

Or potentially it could make sense to hold out a few more years if there are some funds left that were contributed in the last 5 years.

3️⃣ Lifetime rollover cap: $35,000 per beneficiary

This is the maximum that can ever be rolled from 529 to Roth IRA for that beneficiary.

Not per account. Not per parent.

Per beneficiary.

4️⃣ Annual Roth IRA contribution limits still apply

The rollover counts toward the beneficiary’s annual Roth IRA contribution limit.

For 2026, that limit is:

$7,500 per year

$8,500 if age 50+

(Subject to annual inflation adjustments.)

If the beneficiary already contributed $3,000 to their Roth IRA this year, only $4,000 of 529 funds can be rolled over.

No doubling up.

5️⃣ The beneficiary must have earned income

This is not optional.

If they earned $5,000 this year, the maximum rollover this year is $5,000 even though the Roth limit is $7,000.

The earned income rule applies just like a normal Roth contribution.

Step 2: How the Money Actually Moves

This is where logistics matter.

You do NOT:

• Take a distribution to a checking account• Then contribute it manually

That creates a reportable distribution.

Instead:

You request a direct trustee-to-trustee rollover from the 529 plan to the Roth IRA custodian.

Most major custodians now have specific paperwork for “529 to Roth IRA rollover.”

Expect:

• Roth IRA account number required• Beneficiary SSN• Certification that earned income exists• Confirmation that annual limits are not exceeded

This is a clean rollover, not a distribution.

Example:

The 529 Plan is at Fidelity. You want to move it over to a Roth IRA at Vanguard in the name of the beneficiary. Contact Fidelity with the above information to complete their direct trustee-to-trustee rollover paperwork.

What the Tax Forms Look Like

This is where many advisors get tripped up.

You will see two forms.

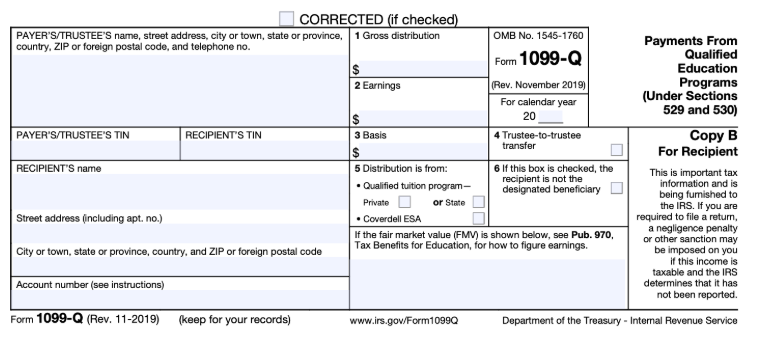

Form 1099-Q (From the 529 Plan)

1099-Q

The 529 custodian issues Form 1099-Q.

Key boxes:

Box 1: Gross distribution

Box 2: Earnings

Box 3: Basis

When properly executed as a qualified rollover to a Roth IRA:

This should be coded as a qualified distribution.

Earnings are not taxable.

If done incorrectly, earnings can become taxable and penalized.

Form 5498 (From the Roth IRA Custodian)

Form 5498

The receiving Roth IRA custodian issues Form 5498.

This reports the contribution amount to the IRS and not by you.

Important:

This rollover shows up as a Roth contribution, not a conversion.

It is not reported on Form 8606. It is not a taxable event.

Step 4: Annual Strategy Planning

Because of the $35,000 lifetime cap and annual contribution limits, this becomes a multi-year planning strategy.

Example:

• Beneficiary age 22• Earns $45,000 per year• Roth limit = $7,000• 529 balance = $40,000

You can roll:

$7,000 in year 1$7,000 in year 2$7,000 in year 3$7,000 in year 4$7,000 in year 5

Total = $35,000

The remaining $5,000 stays in the 529.

This takes five years to fully execute. Furthermore, it can exclude the last 5 years of contributions and earnings.

Subtle Planning Considerations Most People Miss

✔ Coordination with Employer Plans

If the beneficiary is maxing a 401(k), that does not affect Roth IRA eligibility directly but earned income still caps total IRA contribution ability.

✔ State Tax Treatment

Most states follow federal treatment.

Some may not.

If your state gave a deduction or credit for contributions, confirm there is no recapture risk.

✔ FAFSA Impact

Once moved to a Roth IRA:

• It is no longer a 529 asset• Roth IRAs are not counted as assets on FAFSA

That can materially change financial aid positioning.

✔ What Happens if the Beneficiary Does Not Have Earned Income?

You wait. Or consider shifting to a new beneficiary or alternative plan for the 529 proceeds.

You do not force it.

No income = no rollover that year.

What This Is NOT

It is not:

• A way to overfund a Roth IRA

• A way to bypass income phaseouts

• A way to dump $35,000 in one year

• A way to get around earned income rules

It is simply a complex exit ramp for unused 529 funds.

Where This Becomes Powerful

If a child:

• Receives scholarships

• Does not attend graduate school

• Has leftover funds

You now have a way to seed their Roth IRA early.

$35,000 invested at age 22 inside a Roth IRA can be extraordinary over 40+ years for those willing to do the hard work over the 5 years it would take to complete.

Execution Checklist

Before initiating:

☑ Confirm 15-year account age

☑ Confirm no recent 5-year contributions in rollover amount

☑ Confirm earned income for the year☑ Confirm annual contribution space available

☑ Use trustee-to-trustee transfer paperwork

☑ Ensure proper 1099-Q and 5498 filings.

☑ Track lifetime $35,000 cap

Execute each until completed. Document everything.

Final Thought

The headlines make this sound simple.

The mechanics are not. In fact, the amount of rules placed around this are designed to cause people to avoid using this as a strategy.

This is where thoughtful execution matters.

Where a real conversation needs to happen.

Do we use these extra funds for other beneficiaries in the family for their education cost (keeping it in a 529)?

Or do we work through the complexities to get a jump on retirement savings for the current beneficiary?

Both paths have pros and cons. Figuring out your goals will help guide you on the right path.

About the Author:

James Hargrave, MBA, CFP®, CLU® is the founder of Pillar Financial Planning, a fee-only financial planning firm that works with business owners and 1099 professionals.

This article was written in collaboration with Fiduciary Check. If you want to verify whether an advisor is a fiduciary, you can learn more at Fiduciary Check.

Frequently Asked Questions About 529 to Roth IRA Rollovers

Can you roll over a 529 plan to a Roth IRA?

Yes. Starting in 2024, the SECURE 2.0 Act allows certain 529 plan funds to be rolled over to a Roth IRA for the beneficiary of the 529 plan.

However, the rollover must follow several rules, including:

• The 529 plan must have been open at least 15 years • The Roth IRA must belong to the same beneficiary • The beneficiary must have earned income in the year of the rollover • The rollover counts toward the annual Roth IRA contribution limit

What is the maximum amount that can be moved from a 529 to a Roth IRA?

The lifetime maximum rollover is $35,000 per beneficiary.

This means you cannot move more than $35,000 total from a 529 plan into a Roth IRA using this rule.

However, the transfer must still follow annual Roth contribution limits, so it may take several years to move the full amount.

Does the rollover count toward the annual Roth IRA contribution limit?

Yes.

A 529 rollover counts toward the annual Roth IRA contribution limit.

For example:

If the Roth IRA contribution limit is $7,000, the maximum 529 rollover in that year would also be $7,000.

You cannot contribute separately on top of the rollover.

Does the beneficiary need earned income to do the rollover?

Yes.

The beneficiary must have earned income equal to or greater than the amount being rolled over for that year.

For example:

If the rollover is $6,000, the beneficiary must have at least $6,000 of earned income during that tax year.

Are income limits applied like normal Roth IRA contributions?

No.

One major advantage of the 529 rollover rule is that Roth IRA income limits do not apply.

Even if the beneficiary earns above the normal Roth contribution income thresholds, they can still receive the rollover from the 529 plan.

Does changing the 529 beneficiary restart the 15-year clock?

This is currently unclear.

The IRS has not provided detailed guidance on whether changing the beneficiary resets the 15-year requirement.

Because of this uncertainty, many advisors recommend avoiding beneficiary changes shortly before attempting a rollover.

Can recent contributions to the 529 be rolled over?

No.

Any contributions (and the earnings on those contributions) made within the last 5 years are not eligible for the rollover.

Only funds that have been in the 529 plan longer than 5 years can be used.

What tax forms report the rollover?

Two main tax forms are typically involved:

Form 1099-Q Issued by the 529 plan showing the distribution.

Form 5498 Issued by the Roth IRA custodian showing the contribution.

These forms help document that the distribution was properly rolled into the Roth IRA and not treated as a taxable withdrawal.

Who benefits most from this strategy?

This strategy is often most useful when:

• A student receives scholarships • Education costs end up lower than expected • Parents funded a 529 aggressively • A beneficiary finishes school with excess 529 funds

Instead of taking a taxable withdrawal with a 10% penalty, the funds can now help jump-start the beneficiary’s retirement savings.

Is the 529 to Roth rollover always the best option?

Not necessarily.

Other options may still make sense, including:

• Changing the beneficiary • Using funds for graduate school • Saving the account for future education expenses • Using the funds for qualified education expenses later in life

Each situation should be evaluated carefully before initiating a rollover.

Sources

• SECURE 2.0 Act of 2022 – Section 126

• Internal Revenue Code Section 529

• IRS Publication 590-A (Contributions to Individual Retirement Arrangements)

• IRS Form 1099-Q Instructions

• IRS Form 5498 Instructions

Disclaimer

This article is provided for educational purposes only and should not be considered tax, legal, or investment advice. Individual situations vary, and readers should consult a qualified professional before implementing any financial strategy.